The A word

According to the International Monetary Fund’s (IMF) latest World Economic Outlook, the possibility of a ‘double-dip’ recession cannot yet be discounted even if current data show the world economy beginning to recover. The IMF’s main concern is that private demand (including consumer spending) is not showing enough strength to restore consistent global GDP growth by replacing public sector stimulus spending. In this context, it seems almost perverse to raise the prospect of severe product shortages in key technology sectors—nevertheless they now look certain for semiconductors.

Several analysts have been warning of the possibility for some time. One of the most vocal has been Bill McClean, president of IC Insights, and he has since been joined by figures such as Malcolm Penn, chairman and CEO of Future Horizons (who can also point to a background in chip manufacturing).

More to the point, several companies have acknowledged that some (if not all) of their product lines are already being affected. The canary in the coal mine is the historically volatile market for memories, particularly DRAMs and flash. Micron Technology supplies both technologies. Steve Appleton, its chairman and CEO, said this while announcing the company’s Q4 financials: “It appears that industry supply growth and capital spending are at extremely low levels, leaving many products on allocation. We remain optimistic that these trends will continue.”

‘Allocation’, for those unfamiliar with the term, is chip-speak for ‘rationing’. Appleton added that the $750M-$850M that Micron has set aside for capex in the current financial year will be “focused around getting more out of existing facilities.” No new lines and certainly no new fabs will be added as the supply crunch intensifies.

A second-hand rose

One intriguing tale involves Texas Instruments (TI). It recently announced plans to equip a fab shell in Richardson, Texas that was built in 2006 but mothballed. It will manufacture an annual $1B worth of analog semiconductors on 300mm wafers, using second-hand equipment purchased after the bankruptcy earlier this year of memory specialist Qimonda.

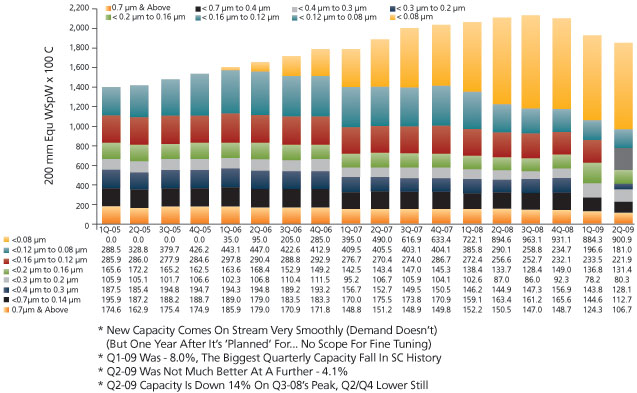

Source: Future Horizons

FIGURE 2 Worldwide MOS wafer fab capacity

Not that long ago, TI announced plans to get out of manufacturing as far as possible and outsource production to third-party foundries, as has the bulk of the semiconductor industry. But this does look at first glance like a very sweet opportunity. “The time is right for this investment,” said Rich Templeton, TI’s chairman, president and CEO. “Customer demand for analog chips is growing, and there’s tremendous desire to save energy and protect the environment.”

Original capex for Richardson was estimated at $3B, albeit under a plan that would have seen it produce digital rather than analog ICs; the equipment being bought from Qimonda is bang up to date but will cost TI just $172.5M. Even given what TI has spent and will have to spend to install, staff and further prepare the site, it still gets the fab for a fraction of its original price.

Also, as one of the foundries’ biggest clients, it has been given some indication of the capacity crunch looming. Its suppliers are already talking about allocation in private and will soon do so in public. So, the ‘fab-lite’ TI became sufficiently concerned about supply chain bottlenecks that it also speeded up the opening of a test and packaging facility for its chips in the Philippines. Richardson is a very cost-effective hedge against the looming problems.

But what are the dynamics behind the existing and incoming shortages, and why do they point to lengthy shortages? There are principally three closely interlinked elements. First, the shape of this recession. Second, the initial response to it as seen across most industries, not just semiconductors. And third, a longer-term factor concerning the growing power of the foundries in the chip business and their financial needs.

V-shaped… probably

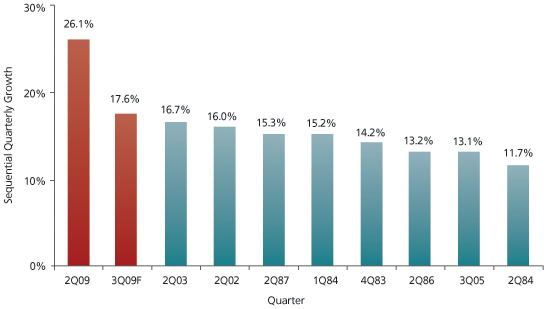

Chip demand has never fallen nor returned so sharply as it has during this recession. For one thing, the last time the world economy suffered so intense a spasm, semiconductors did not exist. According to IC Insights, Q4 of 2008 saw a 21% slump in demand followed by a 20% fall in Q1 of this year. However, this was followed by 26.1% growth in Q2, and Bill McClean is forecasting 17.6% for Q3.

“What you have here is a classic V-shaped recovery curve, albeit a very extreme one, because there’s no other way of saying it—we dove to the bottom,” he says. “Those dynamics alone make shortages inevitable and the numbers for [manufacturing] capacity utilization bear that out further. In Q1 it was about 55%, then about 75% in Q2, and it’s going to be around 90% in Q3.”

Another important wrinkle is then added by the fact that this pattern does not match what has happened in leading markets for finished products with significant chip content. “If you look at PCs, those have been roughly flat. Cell phones are down 5-6%. Flat panel TVs are flat, maybe down 1-2%. Now, those are broad numbers, but what you can say for sure is that relative to the worst global recession in 63 years, end-use demand has held up really well,” says McClean.

The mismatch between supply and demand even when things were bad is clear and is the most obvious factor making long-term shortages now a certainty rather than simply a high risk. However, the depth and length of those shortages is being exacerbated by the nature of the industry’s initial response.

Source: Future Horizons

|

Revenue Per Sq Cm |

2003 |

2004 |

2005 |

2006 |

2007 |

2008 |

|

Chartered |

$3.21 |

$3.29 |

$3.43 |

$3.30 |

$2.79 |

$2.74 |

|

SMIC |

$2.45 |

$3.38 |

$2.80 |

$2.88 |

$2.67 |

$2.68 |

|

TSMC |

$5.04 |

$4.81 |

$4.66 |

$4.25 |

$3.91 |

$3.79 |

|

UMC |

$3.54 |

$4.00 |

$3.22 |

$3.13 |

$2.92 |

$2.81 |

|

Foundry Avg |

$4.22 |

$4.30 |

$3.92 |

$3.71 |

$3.40 |

$3.33 |

|

Industry Avg |

$7.50 |

$8.37 |

$8.48 |

$8.09 |

$7.42 |

$6.96 |

FIGURE 3 Foundry wafer prices at rock bottom

Back on track

Analysts at iSuppli have called the recovery in semiconductor revenues for the current quarter. Although overall 2009 sales are still set to decline by 16.5%, the company said that Q4 revenues will be up 10.6% against the same period last year.

“The seeds of the current recovery were sown in the second quarter,” said Dale Ford, its senior vice president, market intelligence. “During that period, manufacturers began to report positive book-to-bill ratios, indicating future revenue growth. This was followed by another sequential increase in revenue in the third quarter.

“Meanwhile, semiconductor inventories returned to more normal levels in the third quarter after chip suppliers shed stockpiles. They did this by slashing costs dramatically in order to reduce unsold inventory they’d been carrying since the beginning of 2009.”

While these signs are encouraging, and sequential quarterly increases in revenue will continue into 2010, Ford warned that this growth will not be sufficient to lift semiconductor revenues back to pre-recessionary levels until the 2011-2012 time frame.

Furthermore, there remain some worrisome indicators, such as the climbing U.S. unemployment rate, which reached 9.7% in August and is projected to peak at more than 10%. Persistent difficulties in the credit and banking markets as well as the rising number of foreclosures in the U.S. housing market also still cloud the macroeconomic outlook.

Meanwhile, the pattern of a weak first half of the year followed by a strong second will persist into 2010. The company expects to see revenue that is slightly down compared to the Q4 of 2009—but the second half of the year will deliver a strong performance. This will result in 13.8% growth in global semiconductor revenue in 2010, ending the two-year losing streak. Subsequent years will see a return to single-digit percentage growth in the semiconductor industry as conditions stabilize.

Too lean, too mean?

“The industry went into this recession in better shape than it has for any other before,” Future Horizon’s Malcolm Penn told this fall’s International Electronics Forum (IEF). “It was lean, it was mean. But then there was also some panic.”

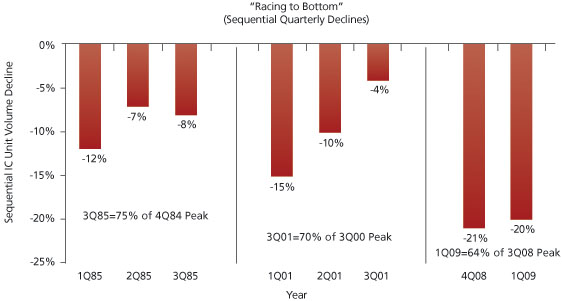

Penn’s data shows that actual output capacity fell by 8% in Q1 of 2009 and then dropped another 4.1% in Q2. “We have never cut back capacity as steeply as this in history,” he continued, going on to also cite the failure of Qimonda. “State-of-the-art 300mm fabs have closed down—this is the good stuff, not the older stuff that you expect to go, and it’s not easy to bring that back online. And there are more fab closures to come.”

Capex numbers tell a similar story. Both Penn and McClean judge this at 12% of sales for 2008, but Penn has it slumping to 7%—another all-time low—in 2009. “And what that means is that it’s not just 2010 where you are going to see tight capacity, but 2011’s written off as well. If all the foundries were to double capex right now that would still bring the 2010 number to only 8%, and that simply isn’t enough,” said Penn. Even where money is spent, it takes time to bring capacity online. “We’re in a business where demand ramps sharply late in the year anyway, typically, around Q3 and Q4 running into Christmas, but you can only ever bring new manufacturing into play very gradually,” says McClean.

A case in point here is TI’s plan for Richardson. The 330 tools it is buying from the Qimonda fire sale, give it all but six of the pieces of equipment it needs. And yet, it began installing the equipment last month, it does not expect chips to come out of the fab until the end of 2010. Even then it will be some time before capacity ramps to the optimum level. And this, remember, is a ‘jump start’ by the standards of chip manufacturing.

The new supply chain

What further compounds this initial brace of issues is the realization that an extended period of shortages is just what some parts of today’s semiconductor supply chain need. “We talk about the boom-bust cycle in semiconductors, and for a long time that is exactly what we had, with periods of over- and under-supply balancing one another out,” says McClean. “But this time, there wasn’t really a boom, in that you didn’t have several years of strong double-digit growth before things went off the cliff.”

In the memory market specifically, volatility was all part of the game. “Companies would enjoy the good years, then the bad ones would come along and almost force them out of business. But then the cycle would start again and save them,” said Penn “Not this time.” Alongside Qimonda, flash supplier Spansion is also currently undergoing a Chapter 11-led restructuring, and only a staggering 60% rise in the average selling price (ASP) of DRAM between January and August may have headed off a complete bloodbath in the sector.

Now, the upward surge in ASPs will allow some manufacturers to catch their breath and restock their war chests. They also need to face the new reality, as identified by another IEF speaker, former STMicroelectronics CEO Pasquale Pistorio, that there is no easy credit—companies are going to have to get much smarter at building, developing and deploying their internal cash resources, and the chip business is very cash hungry.

Source: WSTS/IC Insights

FIGURE 4 History of major IC unit volume adjustments

Source: WSTS/IC Insights

FIGURE 5 Top 10 quarterly IC unit volume growth rates on record

Foundries to get tough on price

However, an even longer standing tension is now coming to the fore: that between the foundries and their various customers. It is a tension that has been there ever since the fabless semiconductor business took off and was followed by one-time integrated device manufacturers shedding much (sometimes all) of their fabs to get “cheaper” and “more cost-effective” services from third-party manufacturers.

Source: TSMC

FIGURE 6 TSMC is expanding Fab12 but similar moves may be rare until 2011

Data from Future Horizons show that all the leading foundries have been getting less revenue per square centimeter of every silicon wafer they produce for at least five years. For the very largest company, Taiwan’s TSMC, a figure that stood at $5.04 in 2003 was $3.79 by 2008 even though the company’s spending on new fab capacity and process R&D was matched by, if anyone, only Intel, the world’s largest chip company.

“Do we expect them [the foundries] to do more for us for less forever? How flawed is this assumption? Aren’t their shareholders going to ask some questions?” Penn offered as a rhetorical flourish during the IEF, because he knows the answer there well enough. “The big winners out of all this will be the foundries, and the biggest winner will be TSMC, because it does have the resources and the others are much smaller,” he said.

McClean shares this view and indeed believes that the process began over a year ago. “It is not as though TSMC has tried to keep its feelings secret—it has made it very clear that the numbers had to improve, and as it has taken a more dominant role in the foundry market, it has acted accordingly. It started to control capex a while ago to make it clear that all the technology it provided, all the IP, all the integration with customers that’s necessary for 32nm and 28nm, all that would have to be paid for.

“They have the market share to push their agenda and it would have been strange if they hadn’t.”

The incoming supply crunch greatly strengthens TSMC’s position. It has significant new capacity coming on stream at Phase 4 of its Fab 12 site in Taiwan. And it therefore has the power to set what it considers a much fairer price. As Penn says, “Get in the queue now guys—you might have a better chance.” The next move in the semiconductor supply chain will only be partly about a recession.

Details on research from Future Horizons and the 2010 International Electronics Forum in Dresden can be found at www.futurehorizons.com. More details about research from IC Insights can be found at www.icinsights.com and from iSuppli at www.isuppli.com.