Go east, young man

Will CES 2010 ultimately be remembered for marking the point where Asia began to drive consumer electronics? Paul Dempsey reports.

It was the Consumer Electronics Show (CES) at which Google ‘did an Apple’ by not doing Vegas, at which the bloggers hyped 3D TV by each individually pointing out how he or she was not getting carried away with it, and at which the gurus claimed to see light at the end of the economic tunnel.

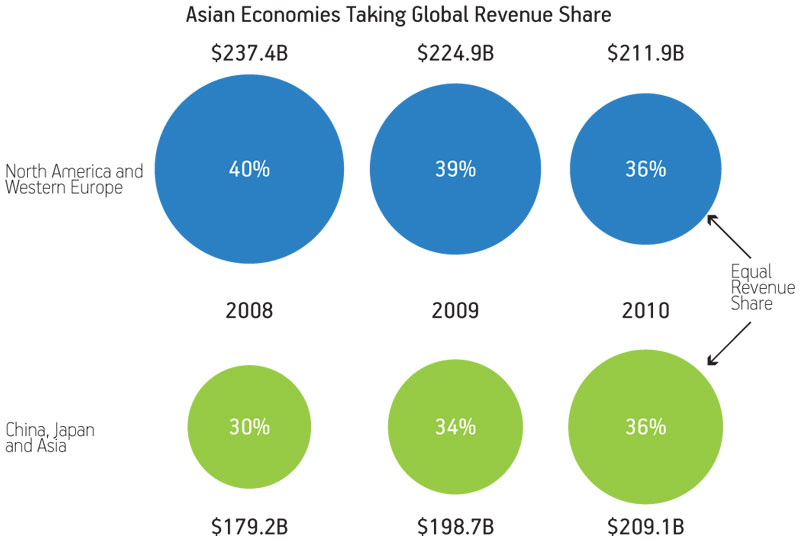

However, none of these may be the biggest ‘takeaway’ from CES 2010. Instead, that honor may go to data that was tucked away before the official show began in a presentation on the global CE market. This will be the first year for which the combined sales forecast covering China, Japan and Asia statistically matches that for North America and Western Europe, at $209.1B vs. $211.9B respectively—both figures translate into a 36% share of sales worldwide (Figure 1).

Figure 1

Regional CE revenue and share of worldwide total. Source: CEA/GfK

These numbers merit being taken seriously because they come from a joint study by organizations with close access to data on worldwide shipments, the U.S. Consumer Electronics Association (CEA) and global market research agency GfK. And while they contain serious qualifications, they do signal a real shift in dominance of the CE market.

It is a shift that raises some interesting questions about CES’ future role as a bellwether for the broadest market trends. Notwithstanding the vagaries of the Japanese market, received wisdom has been that North American tastes will gradually be reflected the world over, fanning out from product launches in Las Vegas (or, in Apple’s and now Google’s cases, at contemporaneous stand-alone shows elsewhere). Even though Europe could be said to have broken this model with its early adoption of cutting-edge mobile communications, this still meant the market drivers came from the western pool.

It is no bad thing in as globalized a sector as electronics for one region to take over from another as the growth leader at the macro level. Many of the leading players throughout the supply chain are Asia-based. But one question being raised—and to which there is as yet no definitive answer—looks at the extent to which eastern tastes and product preferences will continue to take their lead from those initiated in the U.S. and Europe, or take separate directions with major implications for the product mix and feature sets.

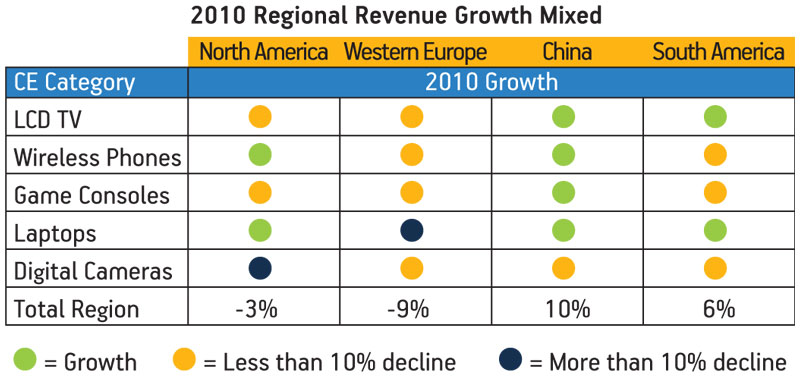

One existing template is Japan. It is long thought to have taken a more gadget-led as opposed to lifestyle-led approach to consumer technologies. That points to potentially radical change and much wider regional differentiation. However, current data have sales growth across emerging markets today concentrated in categories that have reached maturity in established economies (e.g., games consoles, laptops, LCD flat panel displays—Figure 2). The ongoing trend then is more evolutionary.

Figure 2

Regional growth trends in key product categories. Source: CEA/GfK

Another important caveat is that parity is being achieved across the two regions at a time when the west is still very much in recovery, and the numbers are therefore distorted from where they might stand once we return to a period of relative global economic stability.

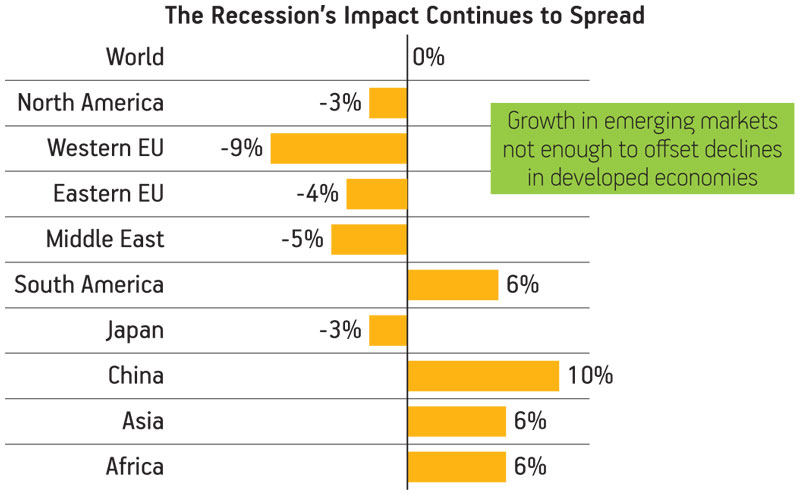

So, for example, 2009 saw North American CE revenues fall by 12%, while those in Western Europe rose only 2%. By contrast, China was up 10%, Asia was up 6% and the mature Japanese market rose by 19%.

The forecast for 2010 is that North American revenues will suffer a further 3% fall, and Western Europe will be down 9%. By contrast, China will again enjoy 10% and Asia 6% growth, while Japan posts a 3% downturn (Figure 3).

Figure 3

Regional revenue growth 2010. Source: CEA/GfK

Comparing the year-on-year retreats in Western Europe and Japan in particular suggests profound market movement, following on from that seen in North America the year before as the global recession gradually spreads in its impact. Today’s economic problems still represent quite a hefty thumb on the scales when you try to extrapolate the numbers.

And there is a third note of caution. In presenting data, Steve Koenig, director of industry analysis for the CEA, said that if you look at the growth across the emerging markets specifically—led by the geographically dispersed ‘BRIC’ quartet of Brazil, Russia, India and China—it does not come close to counterbalancing the declines in sales seen in mature economic blocs.

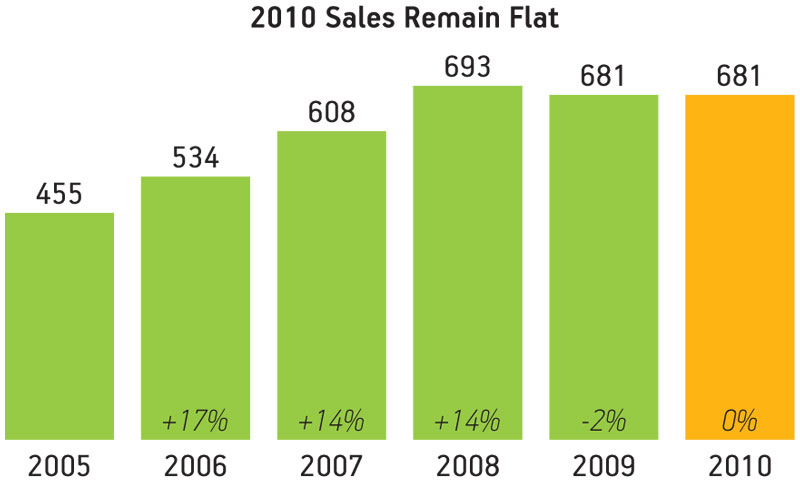

As a result, the global CEA/GfK forecast is for CE sales flat in 2010 at $681B (Figure 4), holding on because some mature markets are still advancing, if only at a slower rate.

Figure 4

Global retail CE sales in $B. Source: CEA/GfK

So can any safe conclusions be drawn? Yes—it is now fair to observe that a regional shift that had been predicted is well under way. China, for example, does not solely need to depend on selling to the developed world to keep its manufacturing sector busy. It demonstrably has an increasingly moneyed middle class that can also purchase much of the CE output from its factories, and it is one that is gaining significant influence. A forecast has become a reality, and it would now be even more foolish to ignore it. Rather, the time to drill still deeper to get a better understanding of these markets has arrived.

At the same time, the arguably local trends that CES offers can still be pushed out to a global model. Moreover, it can be said that these trends have already begun to incorporate the flexibility necessary to cope with the potential for greater regional variations in demand.

In its presentation on the American market, the CEA’s team of chief economist Shawn DuBravac and senior research analyst Ben Arnold identified four technology trends:

- Beyond HD: Tomorrow’s TV Experience

- Content: Connecting and Corralling

- New Screens: Find the Sweet Spot

- Customization & Personalization: Empower the Individual

Digging deeper into all of these, a unifying theme becomes clear. All are linked by varying degrees to how we use the new displays we are all buying for use at home and elsewhere. Taking that further, there is a strong element under which the ‘apps’ model popularized by the iPhone is stretching out onto devices of all shapes and sizes.

Consider ‘Beyond HD’ first. Much of the buzz here has surrounded the fact that 3D broadcasts will be under way not just before the end of the year but before Labor Day. The TVs will be available, and the demos offered by every manufacturer at CES were impressive. But this market is also a long way from maturity (see box).

The CEA says that a little more than 10% of the displays sold this year will be ‘3D ready’—about 4.3M units—rising to 25% by 2013. These are good numbers, and for semiconductor companies specializing in graphics, displays and set-top box capabilities, they point to a healthy emerging market. Nobody is going to turn his nose up at one of those right now—and CES saw NXP Semiconductors, Freescale Semiconductor, AMD, nVidia and Texas Instruments all out in force.

But the noise around 3D has tended to mask what the CEA itself sees as the other half of this trend, the Ethernet-enabled TV. These will make up 20% of shipments this year and more than 50% by 2013. This kind of connectivity allows direct access to ‘apps’ like the video streaming offered by Netflix and Blockbuster, Internet radio from Pandora and—new at CES—Skype audio and video.

Importantly, unlike 3D, extending the display’s capabilities in this way can be done through the after-market. There were as many Web-enabled, media-player set-top boxes as Ethernet TVs on show in Las Vegas. Blu-ray Disc players are also increasingly integrating Internet-delivered services in addition to the format’s own BD-Live technology. And already games consoles have begun to extend their retail stores.

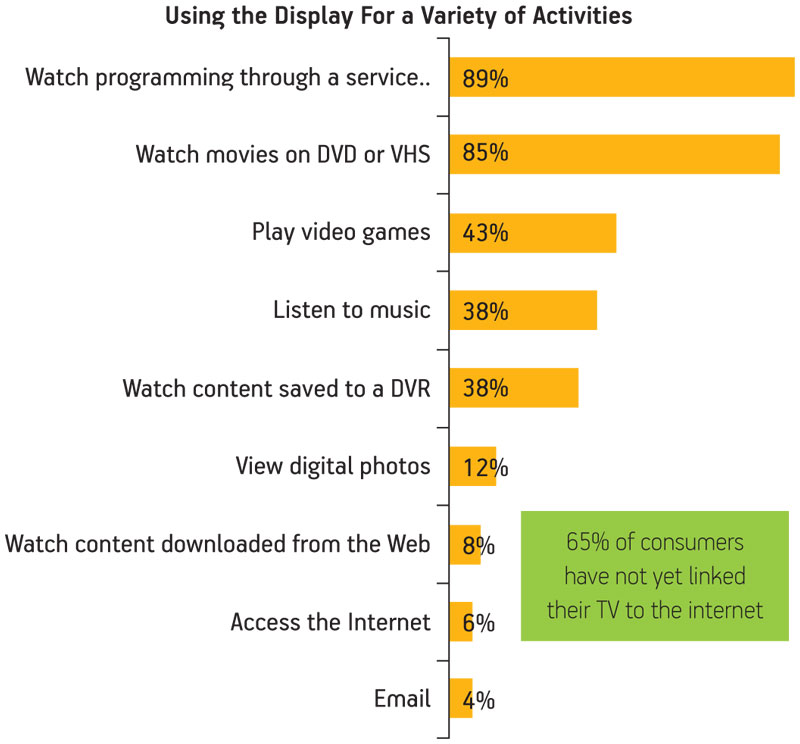

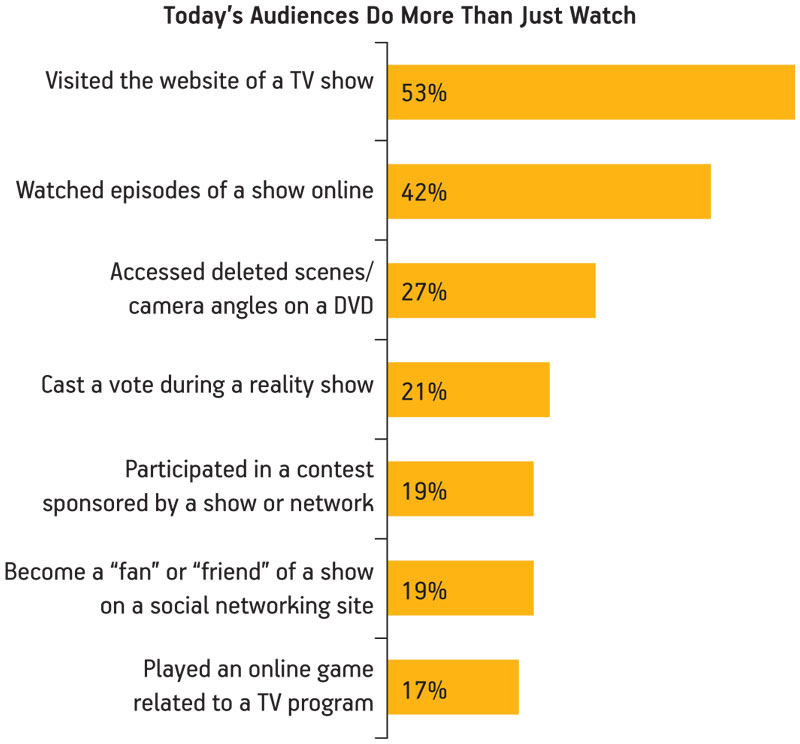

In discussing the second trend, ‘Content’, DuBravac set out the scope of the market offered by connected, apped-up displays by drawing a contrast between the ways in which consumers already interact with media (Figure 5a)—although in many cases via PCs separate from the TV—and how little is being done with the home’s main display at the moment (Figure 5b).

Figure 5b

Using the display. Source: CEA

Figure 5a

The viewing experience beyond the TV. Source: CEA

At the same time, the trend toward cloud storage and the replacement of packaged media by downloads is stimulating customer demands that they should be able to access new or already-owned content across platforms in the home and elsewhere.

The third trend, ‘New Screens’, underlines just where that ‘elsewhere’ is going. We are already familiar with mobile phones at one end of the spectrum, trading up into notebooks, then desktops and ultimately TVs. However, DuBravac noted that there is a gap in this range between 5” and 15”—and it is one that e-readers and netbooks are moving to fill.

The e-book sector is getting increasingly crowded and it seems inevitable that there will be blood on the carpet before long as the likes of Amazon, Sony, Apple, Barnes & Noble and others vie for supremacy. That process could be accelerated by the market’s current attachment to the old ‘walled garden’ revenue model (different e-book formats, exclusive services such as newspaper subscriptions, etc).

This business strategy is also in stark contrast with that proposed for netbooks, which are adopting the much more open approach that has evolved downward from the PC. The fact that netbooks also use—predominantly—either Linux or Microsoft Windows also means that they are more amenable to the extension of the app model.

CEA data has both markets doubling in size and continuing to mature over the course of 2010, but in the longer term, netbooks seem to be poised for the bigger numbers, more than 100M units worldwide by 2013 against 14M for e-readers.

And, of course, Apple has added the iPad. It is concentrating on content consumption rather than creation with its tablet device. The targets are not just the netbook and e-reader, but also portable gaming, mini-DVD players and so on. One distinction could be that while a netbook is often a computer for people who cannot afford full-size laptops, the iPad is for people who do not want full-size laptops.

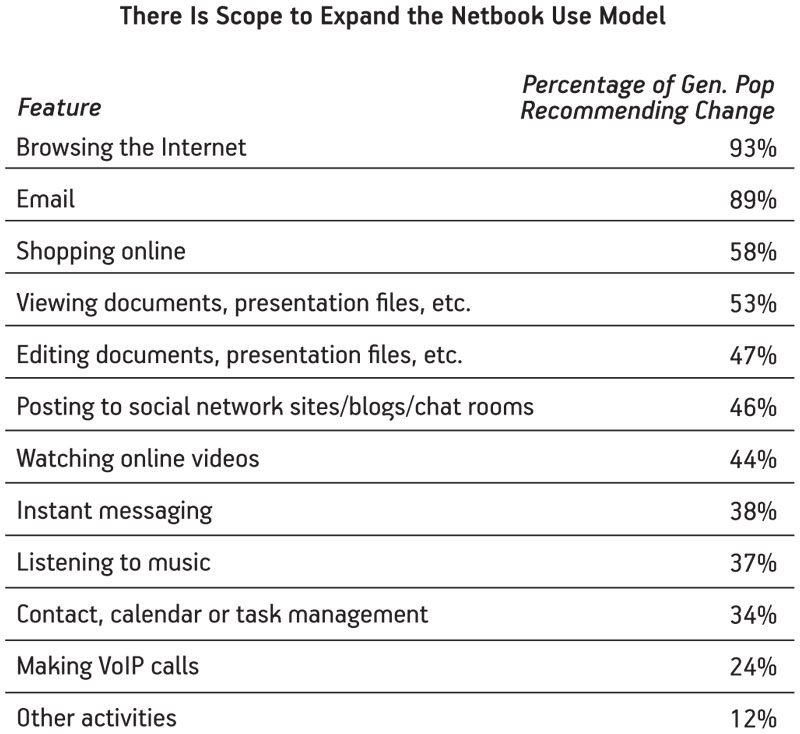

The current use model (Figure 6) also suggests that there is plenty of scope to extend netbooks as new silicon gives them greater battery life and processing power—a consistent theme of presentations from Intel, nVidia, ARM licensees and Qualcomm during CES. The netbook that will let you watch HD content throughout a transatlantic flight should arrive in stores this year.

Figure 6

Netbook usage. Source: CEA

‘Customization & Personalization’ then brings this all together. If the market is fragmenting, changing or simply finding new regional drivers, then basic platforms are just what the doctor ordered. As Windows proved more than a decade ago, sometimes you just have to create the environment in which the user makes the machine do what he or she wants.

More information on the CEA’s research into the US market and its global forecasts, compiled with GfK, can be found online at www.ce.org/research

Fuzzy views on HDTV

Panasonic will ship the first ‘3D ready’ TV this spring, and almost all the major brands aim to have displays on the market before the end of the year. The Consumer Electronics Association forecasts that more than 4M suitably enabled TVs will ship in 2010.

Certainly, some of the historic problems that can wound an incremental technology like 3D are being avoided. Most important of all, there will be content from Day One. The Blu-ray Disc Association has already agreed on a format for 3D HD on packaged media. None has yet been agreed on for broadcast 3D, but both DirecTV (with Panasonic) and a powerful trio of Sony, Discovery Communications and IMAX aim to have channels up and running before the year-end. Meanwhile the UK has already seen its first 3D soccer match, Arsenal taking on the mighty Manchester United.

However, 3D is far from a done deal. There was some very good technology on display at CES, but it was during such a demo that I encountered one of the chip business’ veteran analysts. “Gee,” he said with a grin. “I haven’t seen this much excitement since they launched quadraphonic sound.” In fact, you kept hearing that same ‘joke’.

Things probably are not that bad. In the long term, display manufacturers see 3D more as part of a bigger feature set than a stand-alone sales generator as HD has been. They also see the technology following a traditional adoption curve, pulling in an initial wave of early adopters followed by a lull before the mass market opens up in three or four years.

Part of the problem is that CES 2010 may have marked the beginnings of a recovery, but many players still held back products they did not want to see buried by a recession. This vacuum has been filled by excessive optimism for 3D’s adoption, fueled by the microscopic attention consumer electronics gets in the era of the blogosphere. 3D has gathered both column inches and bits and bytes because there was not ‘enough’ to write about.

As one OEM told me, “This is still a trade show. It’s still about telling the retailers what to get ready for as much as what’s coming out this year. People do forget that.” Silicon vendors are nevertheless well prepared to add 3D capabilities. The systems that will drive next-generation displays do require some refinement and further standards will be helpful (both the SMPTE and MPEG are still working on them). Yet, the fundamentals are in place—most of the debate now surrounds cost-down and integration.

But there is one other thing—those darned glasses. One of the most impressive 3D line-ups already on sale comes from nVidia and is aimed at gamers. CES saw CEO and president Jen-Hsun Huang unveil a special edition of the game based on the blockbuster Avatar. And it’s going to cost several hundred dollars.

The problem here is largely to do with the active-shutter LCD glasses that offer the best 3D HD. These are still costing close to $200 a pair. For the mass market, $100 for a packet of four is seen as the essential price point. To achieve big volumes by 2013, that remains a big challenge.

The shadows lift

U.S. shipments of consumer electronics will reach $165B in 2010, according to the latest forecast from the Consumer Electronics Association (CEA). “2009 is a year none of us wish to repeat,” said CEA president and CEO Gary Shapiro, although he did add that unit shipments actually rose during the worst of the recession by almost 10%. However, this did not compensate for falling prices, which drove revenues down by 7.8%.

In comparison with 2009, 2010 will be virtually flat. However, some products will perform strongly including smartphones (forecast to hit $17B in revenues on 52M shipments) and high-definition Blu-ray Disc players ($1.4B in revenues on 11.5M shipments). One of 2009’s few bright spots, the netbook, will continue to exert a positive influence ($14B in revenues on 30M shipments).

The CEA also published its list of the year’s fastest growing products with the usual rider that many of these are ramping up from very low volumes in 2009.

CEA’s 10 Fastest Growing Products for 2010 Projected growth

- LED Displays 256%

- OLED Displays 236%

- Ethernet-enabled TVs 129%

- e-Readers 127%

- Ethernet-connected receivers 95%

- 3DTVs 95%

- Plasma TVs (60”+) 92%

- LCD TVs (60”+) 85%

- Home-theater-in-a-box (Blu-ray) 84%

- Ethernet-enabled Blu-ray players 74%